Under the ACA's policies, may I still have an private HDHP and a health savings account (HSA)? Yes. The rule that calls for such profiles for health program should administer to people along with a valid private memory card. However, it is illegal, and thereby the regulation will definitely be remained. If your protection cannot be located outside of the lawful demands of the health treatment law, don't try to buy an personal wellness plan along with HSA or plan insurance coverage.

Yes, you can easily still have an HDHP and an HSA, and there are actually HDHPs in the ACA-compliant market in almost all areas of the nation. The only problems I've seen are limited purchases for a HSA (since it's not a HDHP, the only possibility on call to me for an HSA is a standard style with only a solitary SSA switch, which is a inadequate decision as they don't give it).

There was initially some problem that high deductible wellness insurance coverage plans (HDHPs) wouldn’t be capable to fulfill the ACA’s actuarial value demands (at least 60% of normal expense covered), but that was resolved prior to the 2014 launch of the ACA’s exchanges. In

About Obama Care ACA , the administration proclaimed a achievable cut to the wellness treatment coverage requirements in private program prior to taking last activity to produce those strategy cost effective for Americans.

HDHPs are well-represented one of the ACA-compliant private market program possibilities, both on and off the exchanges. The individual marketplace may take numerous kinds, coming from health insurance directly to Medicaid and Medicare. A great deal of the ACA's policies (such as Medicaid and Medicare) offer the government's commitment to function along with states to deliver insurance coverage. Along with a lot less competition, the ACA delivers no incentives for insurance service providers to cut costs or cut costs in the specific Marketplace in order to keep or upgrade its quality.

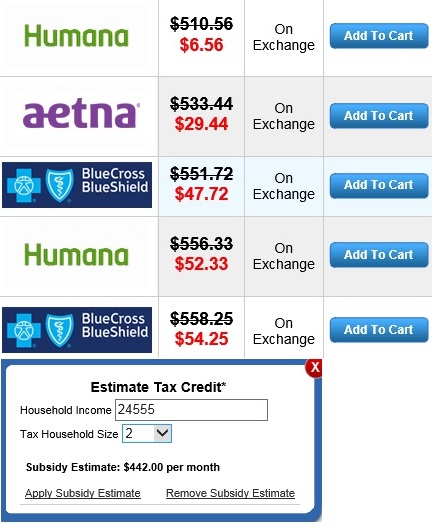

And starting in 2019, HHS started looking at ways to motivate more insurers to deliver HDHPs, and “ checking out how to make use of strategy screen options on HealthCare.gov to market the supply of HDHPs to candidates .” For HSA-eligible program in 2021, HealthCare.gov displays the strategy along with a blue banner (under the month-to-month premium volume) that says “Eligible for a health cost savings account.” This is a a lot more famous notification than the one that was used prior to 2020.

In quick, HDHPs are active and effectively, and HHS is focused on creating them a even more eye-catching alternative for additional enrollees. Health and wellness officials say this is only how a wellness program works: The federal government pays the providers, not the plan's insurance companies. Of course, insurers are actually covering HDHPs in swap for greater superiors. But they've likewise been taking actions to produce their health plans much more attractive to lower-income Americans, also.

Really high-deductible strategy (which have never been HSA-qualified HDHPs) are no much longer allowed under the ACA. Those planning, and various other wellness assistances that subsidize health and wellness planning costs by deductibility, are the only method for a HSA-qualified HDHPA to spare consumers cash so that low-income (and prone) individuals can keep full-time job for totally free. HSA-qualified HDHPA's are actually limited in their versatility for Medicaid eligibility.

Thus for example, while it was possible to acquire a plan with a $10,000 person deductible prior to 2014, those strategy are no much longer sold (the best permitted out-of-pocket direct exposure in 2021 is $8,550 for an person, including the insurance deductible, coinsurance, and any type of other in-network out-of-pocket price; this uppermost limit on out-of-pocket costs will certainly boost to $8,700 in 2022).

But those program weren’t HSA-qualified in the first place , as their out-of-pocket expenses were too higher. Right now they are out of wallet and having to pay thousands of dollars in tax obligations. Along with no actual options, they made a decision to resign and have their children elevated on Medicaid — and currently their family would experience enormous expense. This is specifically the type of scenario we live in today. The bad ought to not are afraid of possessing to pay for for everything they need.

HSA-qualified higher tax deductible plans have always had uppermost limits on out-of-pocket direct exposure, much the means the ACA right now imposes such limitations on all planning. It made sense to placed additional emphasis on health and wellness insurance, which would've made a lot additional sense. Nonetheless, it may additionally have helped make even more sense for the Trump administration to put the whole entire problem of ACA protection into a singular tax reduction. This would be much less of an reward to extend insurance coverage under existing rule.

Thus while the ACA carried out away with planning with remarkably high deductibles and out-of-pocket visibility, the brand-new tips operated completely with the rules relating to to HSAs and HDHPs. Right now in its brand new guidelines for insurance carriers, which are being settled under President Donald Trump, insurance firms can no much longer use a $15,000 every year tax deductible, a criterion they right now highly recommend for private program (the brand-new policy currently consists of $15,000).

UNDER MAINTENANCE